Price Impact on Uniswap V3

A visual summary of a master's thesis on DEX price impact and private order flow.

Price Impact on Uniswap V3

A short visual guide to the thesis, for readers who want the research question, method, and conclusions without reading the full dissertation first.

Full thesis: Tesi_Stampa.pdf

Code: Univ2+Univ3

LaTeX source: thesis_tex

The Question

Decentralized exchanges do not work like traditional limit order book markets. Uniswap executes trades against an automated market maker curve, while Ethereum orders transactions in discrete blocks. Between submission and execution, some transactions are visible in public mempools and others travel through private routes.

The thesis asks two empirical questions:

- How much does an ETH-USDC swap permanently move the Uniswap V3 price?

- Does private order flow contain more price-relevant information than public mempool-observed flow?

The short answer is: yes, private order flow appears to be much more informative in this sample.

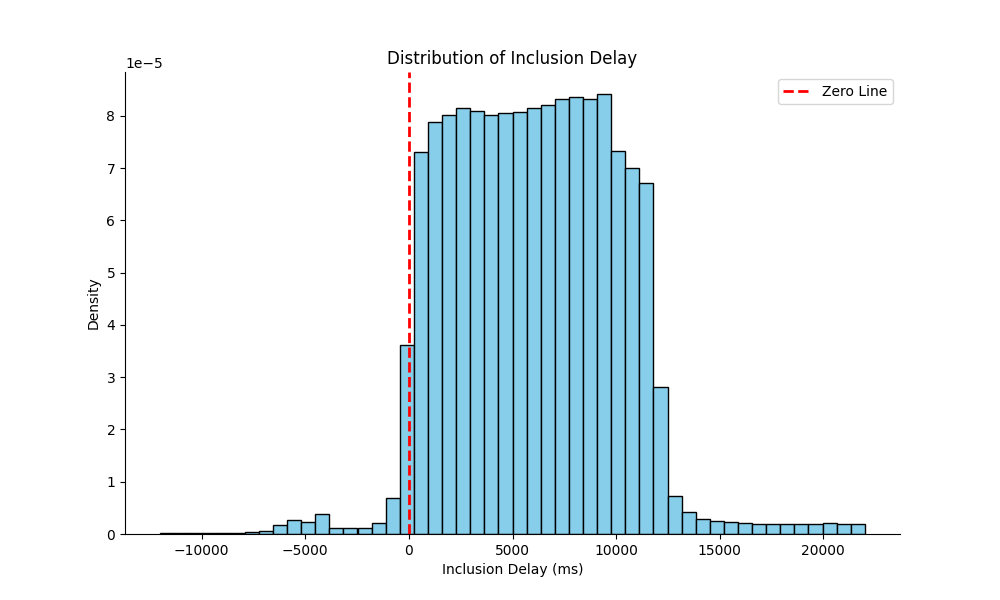

Data In One Picture

The analysis focuses on ETH-USDC Uniswap trading and combines on-chain swap events with public mempool observations. A swap is treated as public when it is observed before block inclusion in public mempool data. If it is not observed there, it is classified as private order flow.

This classification is empirical and collector-dependent: not seeing a transaction in public mempool data is evidence of private routing, not a perfect proof of every private channel used.

The inclusion-delay distribution captures the timing gap between public mempool visibility and block inclusion. This timing matters because the VAR uses transaction ordering to infer how trades and returns interact over short horizons.

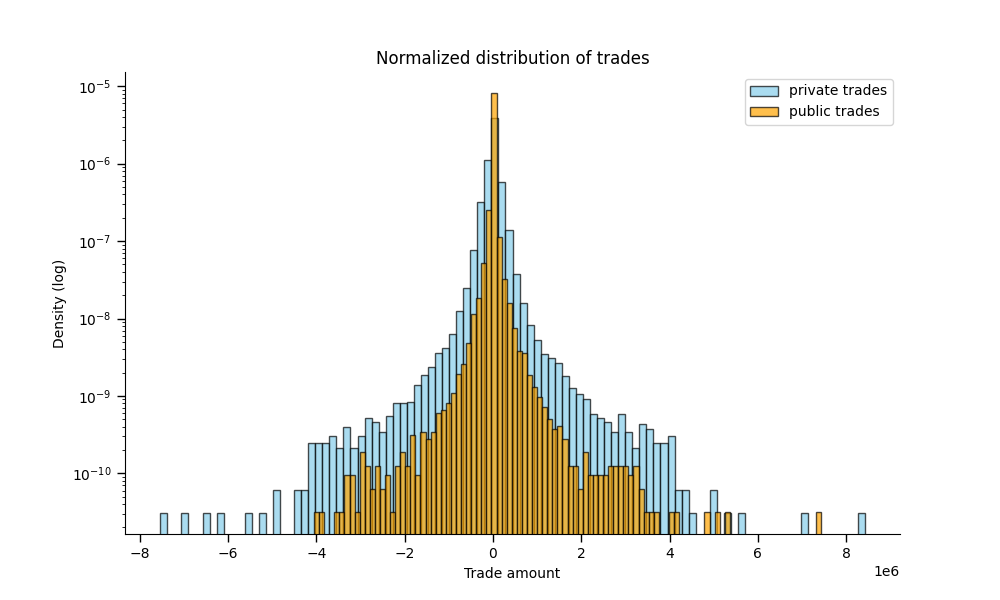

Why Order Flow Type Matters

Public order flow is visible before execution. Searchers, builders, and other sophisticated agents can react to it. Private order flow is less broadly visible before block publication, so it can carry different information and produce different price-discovery dynamics.

Private order flow has heavier tails in the trade-size distribution. That is consistent with the economic intuition that more sophisticated or informed actors may route larger trades privately.

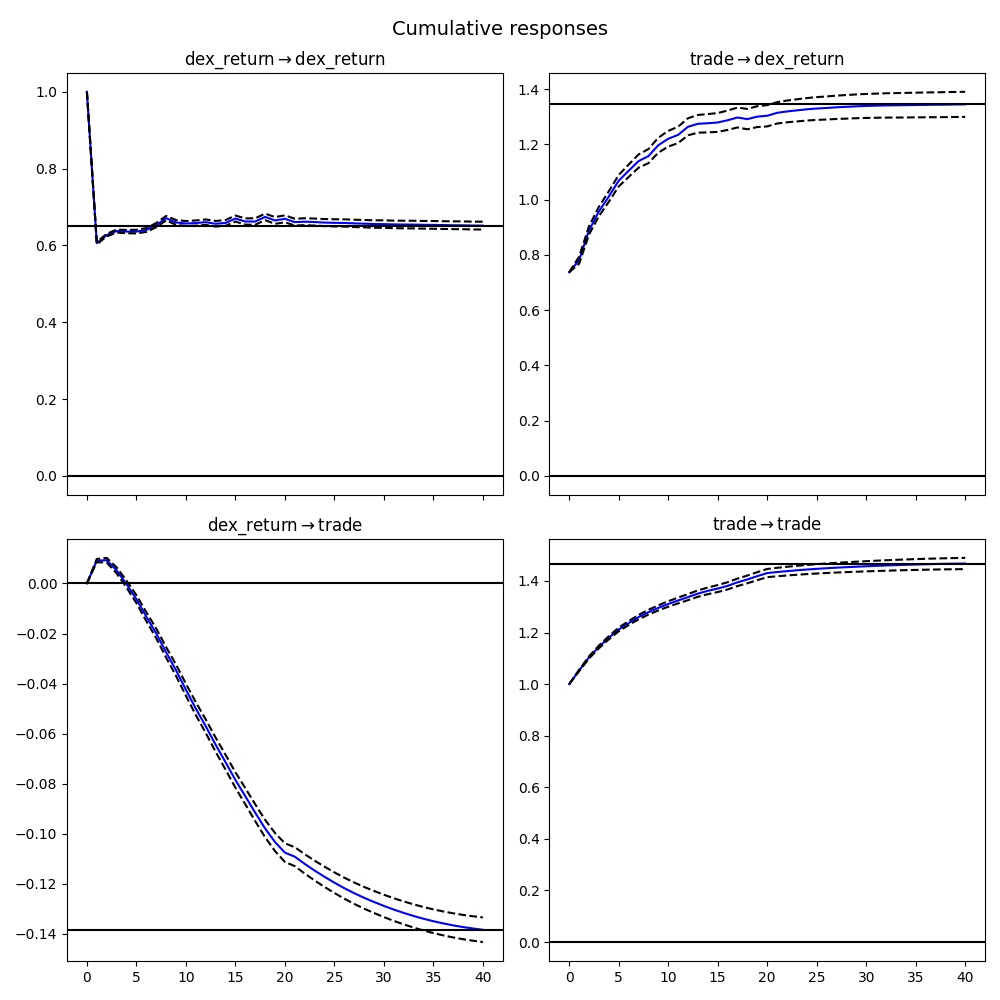

Method

The empirical model is a structural vector autoregression. In the baseline two-variable model, returns and signed trades are modeled jointly:

returns_t = f(past returns, past trades, contemporaneous trade shock)

trades_t = f(past returns, past trades)

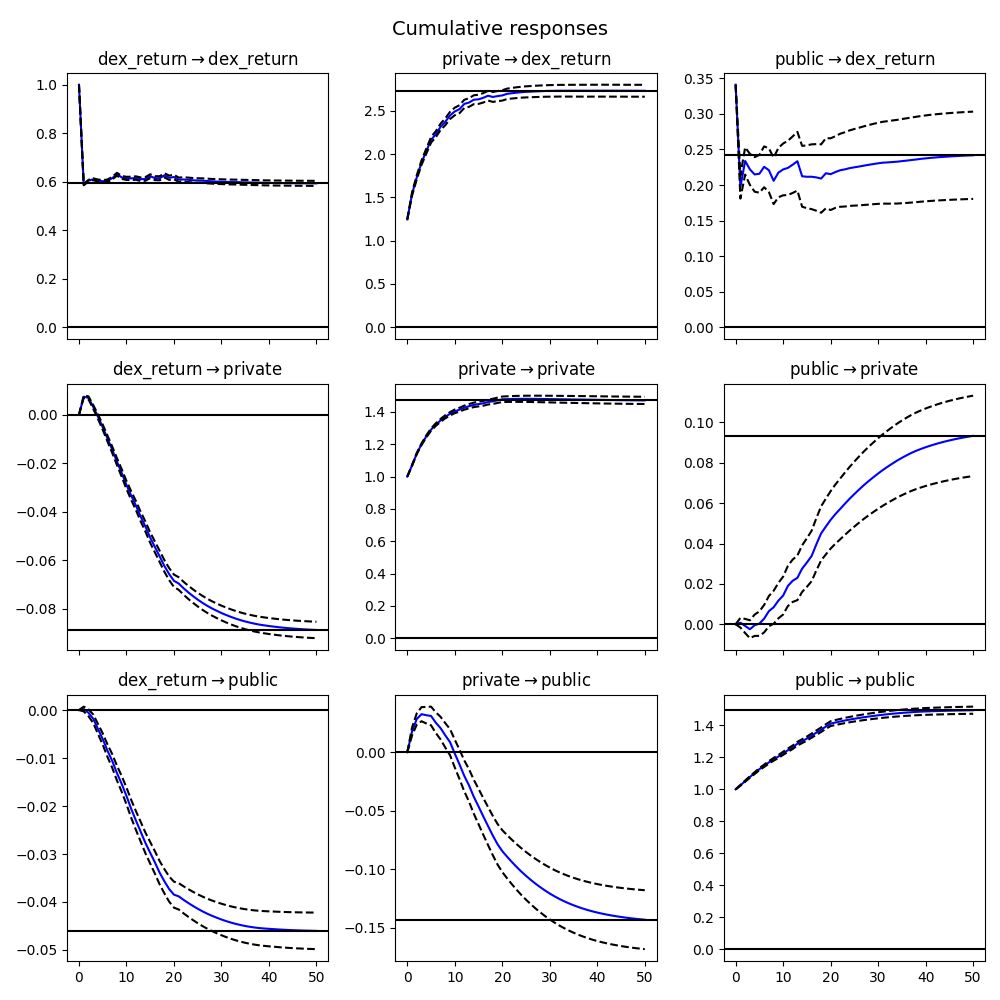

The thesis then expands this into a three-variable model that separates public and private trade signs:

returns_t = f(past returns, past private flow, past public flow)

private_t = f(past returns, past private flow, past public flow)

public_t = f(past returns, past private flow, past public flow)

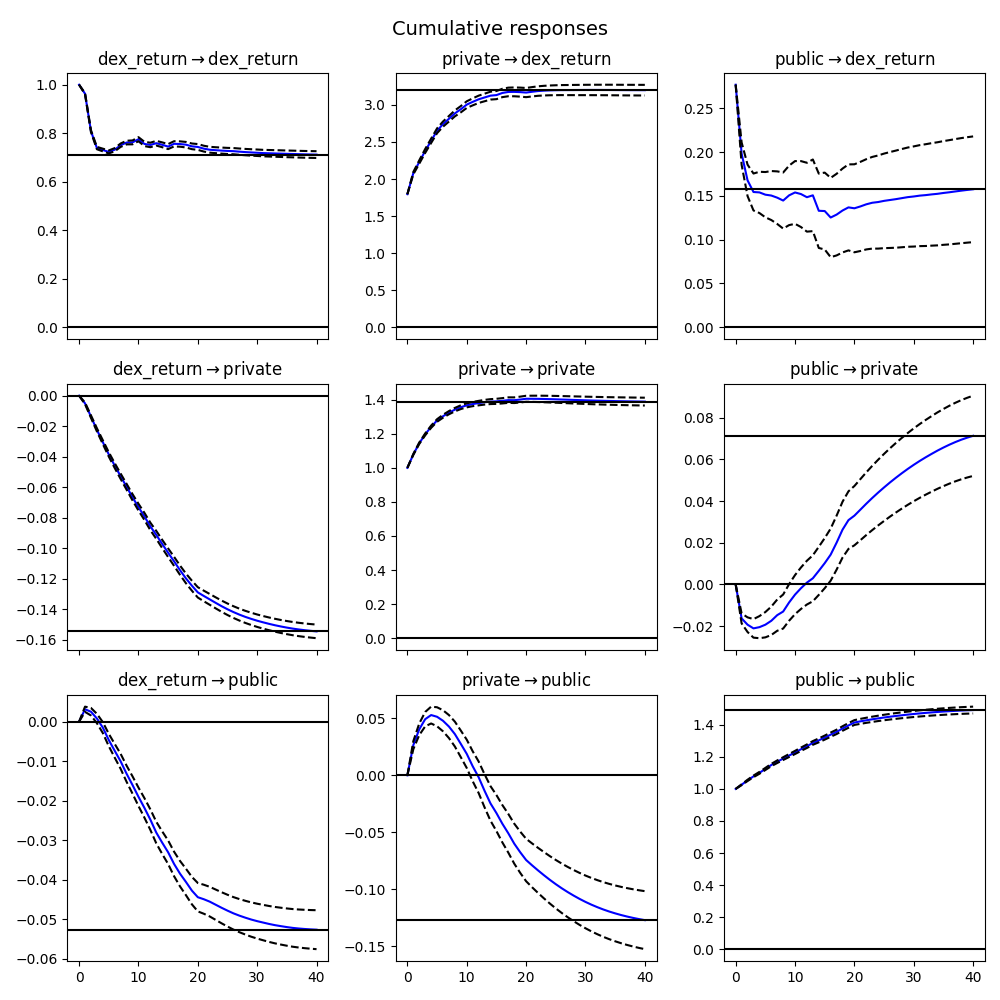

The main object of interest is the cumulative impulse response: after a signed buy shock, how much of the price move remains after subsequent trades and returns have propagated through the system?

Result 1: Trades Have Persistent Price Impact

In the baseline VAR, a trade-sign shock has an estimated permanent price impact of about 1.345 basis points.

This impact decomposes into two channels:

- 0.737344 b.p., about 55%, is contemporaneous and mechanical.

- The remaining 45% is linked to correlated future order flow.

That split is important. In an AMM, part of price impact comes directly from the pricing curve. The rest comes from what follows the trade.

Result 2: Private Flow Is More Informative

When public and private order flow are modeled separately, private order flow has a much larger permanent impact on returns.

The three-equation VAR estimates:

| Shock | Permanent impact on return |

|---|---|

| Private trade flow | 2.728 b.p. |

| Public trade flow | 0.2452 b.p. |

The contemporaneous coefficients also differ:

| Shock | Contemporaneous impact on return |

|---|---|

| Private trade flow | 1.245481 b.p. |

| Public trade flow | 0.341109 b.p. |

The interpretation is that private trades in this ETH-USDC sample reveal more price-relevant information than public mempool-observed trades.

Result 3: Public Flow Can Trigger Private Reaction

The model also suggests cross-flow dynamics. Public swaps can be followed by private order flow in the same direction, while the reverse relation weakens or turns negative after a few lags.

A plausible market-structure explanation is that sophisticated agents observe public mempool trades and respond before or around execution, for example through directional trading, backrunning, or other MEV-related strategies.

The thesis also checks robustness by changing the ordering convention from mempool publication time to block execution order.

The price-impact pattern remains meaningful, but some attribution between public and private flow changes. This is expected: in Ethereum, the timestamp at which a transaction becomes observable and the position in the final block are economically different objects.

Market Context

Uniswap liquidity is not uniformly available at every price. Concentrated liquidity changes the price response to trades, especially when execution crosses active liquidity ranges.

The thesis treats this as part of the market microstructure: AMM design, Ethereum transaction supply chains, and public/private order flow jointly shape observed price discovery.

What This Contributes

This work connects three areas that are often studied separately:

- Decentralized exchange microstructure.

- Ethereum mempool and private order-flow routing.

- Structural VAR methods for price impact and information content.

The empirical takeaway is that transaction visibility is not a minor technical detail. In this sample, public versus private routing is directly related to measured information content and price impact.

Limitations

- The empirical sample focuses on ETH-USDC Uniswap trading, so results should not be generalized mechanically to every AMM, token pair, or market period.

- Public/private classification depends on available mempool collectors.

- The VAR is linear and uses constant parameters, so it does not fully capture regime changes, nonlinear liquidity, or changing market conditions.

- Some scripts require external RPC providers and large raw CSV datasets that are not committed to this repository.

Next Steps

The natural extensions are:

- Repeat the analysis across more pools and DEX venues.

- Separate benign private routing from explicitly toxic order flow such as sandwiching and frontrunning.

- Estimate time-varying or regime-dependent impacts.

- Package the extraction and modeling pipeline into a reproducible command-line workflow.

For the complete derivation, tables, references, and robustness checks, read the full thesis PDF.